Let’s be honest. Buying health insurance in India feels a lot like walking into a spice market blindfolded. There are too many choices, everything smells slightly overwhelming, and if you aren’t careful, you end up with something that burns a hole in your pocket when you actually try to use it.

I remember sitting with my uncle in a crowded Mumbai hospital café a couple of years ago. He was waiting for his wife’s discharge papers, completely exhausted, holding a bill that was nearly double what he expected. Why? Because he had blindly bought a policy based on a low premium without looking at the fine print. That was the day I realized that figuring out How to Choose the Right Health Insurance Plan isn’t just a financial chore it’s a critical life skill.

So, grab a cup of chai, and let’s break down exactly how to navigate this maze without getting ripped off. No heavy corporate jargon, just a straight-to-the-point, real-world guide from someone who has been in those hospital corridors.

Why We Fall for the Wrong Policy | The Psychology of the Premium Trap

Here’s the thing: our natural instinct is to look at the price tag first. We hunt for the lowest health insurance premium , pat ourselves on the back for saving money, and store the PDF away in an email folder we’ll never open again. But that cheap policy is often cheap for a reason.

Right now, medical inflation in India is skyrocketing at an alarming rate of nearly 14% to 15% annually. A simple room in a decent private hospital that cost ₹5,000 a night a few years ago can easily set you back ₹10,000 today. If you choose a weak policy just because the yearly premium was low, you are essentially agreeing to pay a massive chunk of your savings when a crisis hits.

What fascinates me is how we treat insurance like a tax-saving tool rather than an actual shield. We buy it in a rush in March, pick a basic individual health insurance plan, and hope for the best. But when you are dealing with a real medical emergency, tax deductions are the last thing on your mind. You want peace of mind, and that only comes when you know the insurer actually has your back.

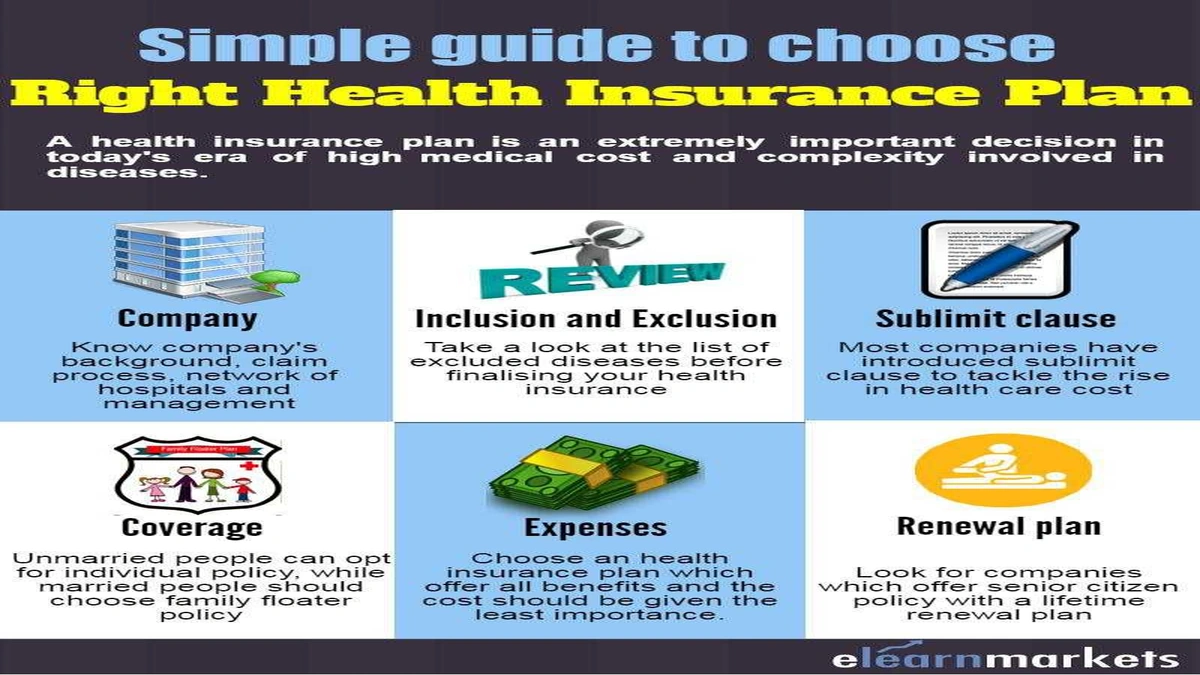

The Step-by-Step Blueprint | Demystifying the Fine Print

Before you even look at a single brochure, you need to understand that a policy is only as good as its hidden clauses. If you are planning your financial future while you explore digital avenues on aninnovative tech platformto manage your cash flows, securing your health should be your very first step. Let’s look at the critical checkpoints you must analyze:

1. Check the Waiting Period for Pre-Existing Diseases

Let’s say you have high blood pressure or diabetes. In the insurance world, these are classified aspre-existing diseases. You can’t just buy a policy today and claim expenses for these conditions tomorrow.There is always a waiting period in health insurance that can range from 1 to 4 years. According to the latestIRDAI guidelines, insurers are streamlining these timelines, but you still need to actively seek out plans that offer the shortest waiting periods if you have ongoing health issues.

2. Watch Out for the Room Rent Limit

This is the silent killer of hospital bills. Many plans cap your daily room rent to 1% of your total sum insured. If you have a ₹5 Lakh cover, your room rent limit is ₹5,000 per day.

But here’s the catch: if you admit yourself to a room that costs ₹8,000 per day, the insurance company won’t just ask you to pay the ₹3,000 difference. They will apply a “proportionate deduction” to your entire bill including surgeon fees, ICU charges, and diagnostics. Yes, you read that right. Your entire claim gets slashed proportionally. Always try to choose a policy with no room rent limit.

The Hidden Triple Threats | Room Rent, Co-Pay, and Restoration

When you are looking to buy the best health insurance policy , you will run into three terms that can make or break your claims experience: the co-payment clause, restoration benefits, and the no-claim bonus. Let’s demystify them.

A co-payment clause is an agreement where you pay a fixed percentage (say 10% or 20%) of every single claim, and the insurer pays the rest. While this lowers your annual premium, it is a terrible deal unless you are a senior citizen who has no other options. If your bill is ₹10 Lakhs, a 20% co-pay means you have to scrape together ₹2 Lakhs from your own pocket. Avoid it if you can.

On the flip side, look for a policy that offers a robust restoration benefit . Imagine you have a ₹10 Lakh policy, and you exhaust the entire amount treating an illness. If another family member falls sick later that same year, a restoration benefit automatically reloads your cover back to ₹10 Lakhs at no extra cost. It’s like having an emergency backup battery for your health cover.

And don’t overlook the no-claim bonus . If you stay healthy and don’t make a claim during the year, quality insurers will reward you by increasing your sum insured by 10% to 50% for the next year without raising your premium. It’s a fantastic way to naturally beat medical inflation.

The Golden Checklist | How to Tailor the Policy to Your Family

There is no one-size-fits-all plan. What works for a 25-year-old fitness enthusiast living in Bengaluru won’t work for a family of four in Jaipur. Choosing a policy is much like setting up a safety net when transitioning to thebest remote jobs beginners 2026offers; it requires assessing your specific lifestyle and risks.

If you have dependents, a family floater plan is usually the most cost-effective way to cover everyone under a single, shared umbrella. However, if you have elderly parents, buy them a separate policy. Mixing elderly parents with young children in a single floater plan drives up the premium for everyone based on the oldest member’s risk profile.

Next, evaluate the network of cashless network hospitals . Check if the major hospitals near your house have an active tie-up with the insurer. Trust me, the last thing you want to do during a medical emergency is run around arranging lakhs of cash to pay the bill and then wait months for reimbursement.

Finally, consider adding a critical illness rider to your base plan. While standard health insurance covers hospital bills, a critical illness rider pays out a lump sum amount upon diagnosis of severe conditions like cancer or kidney failure, helping you cover daily living expenses while you recover.

Frequently Asked Questions about Choosing Health Insurance

Can I buy a health policy if I already have corporate insurance?

Yes, and you absolutely should. Corporate health insurance is only valid as long as you are employed at that specific company. If you lose your job, decide to take a career break, or retire, you will instantly be left without any cover. Buying an independent plan early ensures you build up your waiting periods while you are still healthy.

What is cashless hospitalization and how does it work?

Cashless hospitalization allows you to undergo medical treatment without paying the hospital directly. The insurance company settles the bills directly with the hospital, provided the hospital is part of their network and the treatment is covered under your policy guidelines.

Does health insurance cover maternity expenses?

Some plans do, but they usually come with a waiting period of 2 to 4 years and have specific sub-limits. If you plan to start a family soon, look for policies that offer maternity cover with shorter waiting periods, but be prepared for a slightly higher premium.

How long is the typical waiting period for pre-existing diseases?

Generally, the waiting period for pre-existing conditions like diabetes, hypertension, or asthma ranges between 2 to 4 years. However, some modern plans allow you to reduce this waiting period to 1 year by paying an additional premium.

What is a restoration benefit in health insurance?

A restoration benefit is a feature that automatically restores your policy’s sum insured to its original amount if it gets exhausted during a policy year. This is highly beneficial for family floater plans where multiple members might require hospitalization in the same year.

A Final Insight for Your Peace of Mind

At the end of the day, health insurance isn’t about expecting the worst; it’s about protecting the life you are working so hard to build. Don’t rush the process. Read the policy wordings, ask tough questions to your agent, and never hide your medical history just to get a cheaper premium. It is always better to be rejected at the application stage than to have your claim rejected at the hospital bed. Take charge of your health coverage today, and breathe a little easier tomorrow.